(First published in the April 19, 2018 issue of City Pages)

Got a personal budget? There’s a free class for that and more

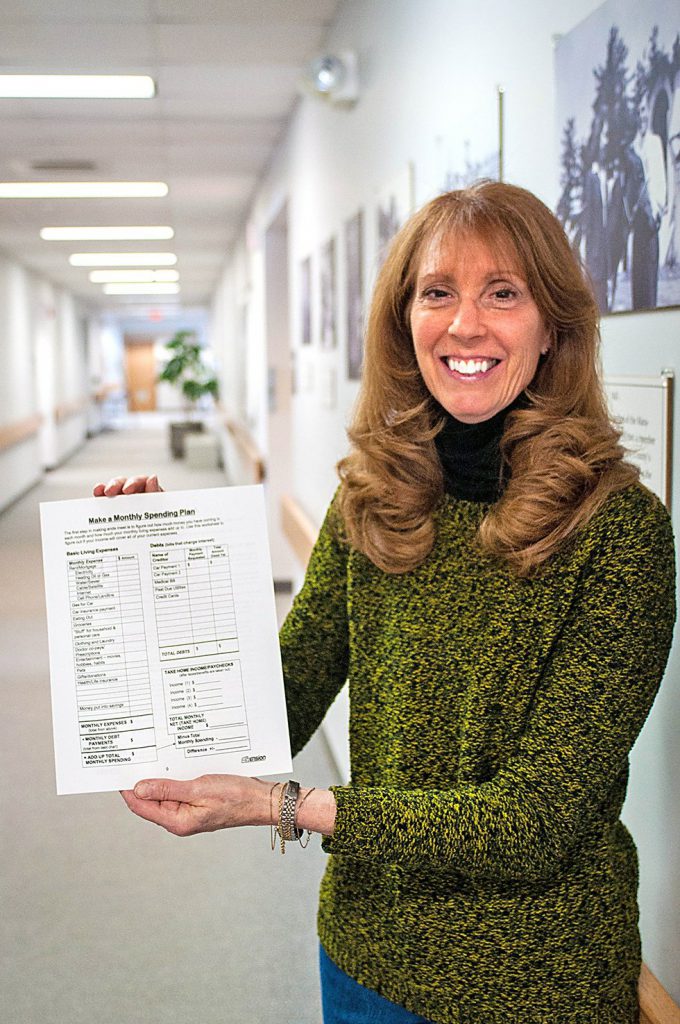

Pam Anderson of the Get Smart Wausau Coalition, with a sample of a worksheet from one of several personal finance classes the coalition helps present throughout the year.

A meme that caught my attention recently: I am torn between saving money and “You Only Live Once.”

It was funny timing because I had just sat down with a frugal friend to discuss my new work-in-progress household budget, how I could start improving my spending habits, and his ideas on how this whole personal budgeting thing works. He even gave me tips on how he squirrels away money and what I need to do to save for fun things like travel abroad or for any emergencies that might arise (like a dead water heater, did you read my story in last week’s issue?).

Like a lot of people, my “budget” was basically this: Buy everything with a debit card and balance my checking and savings account when the mood struck; and slap big ticket fun stuff like trips on a credit card.

I didn’t track where I was spending or on what. I was, you could say, in the “You Only Live Once” frame of mind.

But for this article about personal finance resources in Wausau, I recently attended a UW-Extension budgeting class at the Marathon County Public Library. The basics of the workshop further convinced me that having my bank account blowing in the wind every month was in reality not fun at all. I looked at some apps online, settled with Everydollar.com and began crafting my budget.

My friend and I discussed how little things add up. We looked at where I could pare down some spending: like on cosmetics, clothing, and monthly app subscription fees. By not spending just $6 a day, I could save up $2,190 a year—the equivalent of a round-trip plane ticket to France.

When presented that way, a daily coffee run doesn’t seem worth it. I’d rather save now and drink a cappuccino on the Champs-Elysees in 2019—that’s how you achieve “you only live once” experiences.

Going further, that $6 a day adds up to almost $11,000 in five years.

Sounds obvious, right?

It sure is. But only when you take time to actually think about it and write down the numbers.

Which, rather than magic bullets, is the point of any budgeting process, including the many personal finance workshops organized by the Marathon County UW-Extension and Get Smart Wausau Coalition (a group of banking, nonprofit, and related-field professionals).

Everyone can benefit from creating and sticking to a budget, no matter their socioeconomic status, says Leah Griesbach, a financial wellness advocate at Catholic Charities in Wausau, which leads many of these local programs. “Some people we see have massive amounts of debt, some have bad credit, some are going through the eviction process and are looking for affordable housing… Financial literacy is a learned behavior. Without an example, there is no way for people to know how to track their spending, cut expenses, or better their credit.”

When individuals or families don’t practice healthy money habits, just one incident or situation—medical debt, student loans, or excessive use of credit—can send them into a vicious downward spiral.

“We would love to see more families and individuals come to us before they find themselves in financial distress,” says Griesbach, who helps teach budgeting workshops, which are free and useful to anyone looking to better their financial situation.

The budgeting classes try to help individuals and families evaluate their relationship with money and identify spending habits. “The importance of developing a spending plan, how to track spending, how small expenses can really add up, and setting financial goals.”

“Budgeting education is not just for those who need temporary assistance, it’s a skill, that once learned, can benefit them for the rest of their life,” she says.

Anyone can utilize their services and budgeting benefits everybody. In addition the workshops held at the library in Wausau and UW-Extension, Catholic Charities provides one-on-one financial coaching. “We welcome all who come to our door. Monday is our walk-in day, no appointment is necessary; however, if individuals needing assistance aren’t able to come in on Mondays we recommend they give our office a call,” Griesbach says.

One couple’s experience: Rocky at first, but payoffs come quickly

In their early 30s, John and Michelle Phillips of Weston now have a pretty good handle on their household budget, but it wasn’t always easy. One of their strategies is a focused effort to pay down loans and credit with the goal of being debt-free in the near future.

They’ve cut down on extras like cable TV, but Michelle Phillips knows that a few years of being frugal will pay off in the end. People tend to get in financial trouble by overspending and using credit just to keep up appearances. “You’re trying to keep up with the Joneses and the Joneses are broke,” she says.

Years back, Michelle’s mom gave the couple the book, The Total Money Makeover, by Dave Ramsey. “We scoffed at it. We thought we knew how to save and spend money so we blew it off,” Michelle says.

But since then the Phillips had children and went from a dual- to single-income family, with Michelle staying home. In February 2017, the couple decided to give intentional budgeting another whirl. She’s happy to report that their effort is paying off already.

They worked off the Ramsey book’s seven “baby steps” toward financial health. The first is to save $1,000 as an emergency fund for unexpected expenses, like vehicle repair. Next comes paying off all consumer debt, student loans, car payments and personal lines of credit—basically everything except a mortgage. The final step in his plan is to be completely free of debt so that you can build wealth.

“We are super close to paying off all debt,” says Phillips. They visualize the strategy as a snowball effect of accumulating payments: When one debt is wiped out, the money for that payment gets rolled into paying down the next debt, and so on. “It starts as a tiny snowball,” says Phillips, but soon these increasing payments are moving faster toward your goal.

For example if you owe $50 on a Victoria’s Secret card you pay that off. Then you devote what would have been that payment toward more quickly paying off, say, the $300 balance on your Target account. You then move onto the next debt with those two monthly payments combined.

Phillips admits the whole budgeting and spending plan process was rocky at first. “Ramsey says finances are one of the biggest arguments in relationships and that’s very accurate. Finances are hard. Sometimes we can be judgmental about others’ spending,” she says.

During the couple’s first three months on the plan, Michelle and John had to work very hard to always talk about how each of them spent money. “We really had to stretch things. All our extra money went to debt and we were short in other areas if we weren’t communicating,” she says.

Eschewing fun stuff and instant gratification isn’t easy. What helps is that the Phillips created a bare bones budget to work from, which includes recurring bills like the mortgage, electricity payments, groceries and gas. “We have those set amounts and if there’s ever anything leftover, it gets thrown into the next month’s budget,” she says.

To meet their goals, Phillips gave up some personal luxuries like having her eyebrows professionally waxed. She now dyes her own hair and goes to the Beauty College for haircuts.

You can choose cheaper ways to do the things you value, she says, or just cut back. “It’s about giving yourself the financial freedom to have choices. You just have to sacrifice short term… It’s like talking to your inner six year old. You have to have a little self control.”

Resources for all ages

The underlying principal of the Get Smart Wausau Coalition is that helping individuals become more financially sound and stable, helps the whole community, says Pam Anderson, a retired banker who chairs the group.

The coalition of volunteer educators, financial institutions, non-profit agencies, the city of Wausau, and other for-profit businesses, all work together to give free or low cost education.

They believe the resources they put into the coalition can make a big picture impact. “If you have individuals living in the community who are struggling financially, you don’t have a strong community,” says Anderson. “The community needs to be strong… when you have children in families who are struggling with paying for food, that young person doesn’t learn as well as somebody who comes from an environment where they are healthy and have a strong situation. Financial knowledge in using the funds you have to the best of your ability creates that stable community.”

Financial counseling classes are done throughout the year, including workshops geared specifically toward:

• Budgeting and living expenses

• Credit, and wise use of credit

• Renting and how to be a good tenant

• Debt in general

• How to keep your money safe

• Identity theft

• Home ownership education

The coalition also organizes an annual day-long event. “When we do the financial wellness conference, we provide free copies of attendees’ credit reports and credit scores then they can sit with somebody to go over it,” says Anderson.

Credit scores have a huge impact on our lives, from the cost of car insurance to landlords looking at the scores to see if somebody pays bills on time, Anderson warns. “Thirty years ago it wasn’t even around, but today it’s a primary driver… on a number of different aspects in life.”

The coalition even aims to educate kids. For Money Smart Week beginning April 22, the coalition heads out to libraries and Head Start programs to read books to children with a subtle message about financial stability and budgeting.

For people who are middle aged, Anderson says the number one issue is saving for retirement. “Many times we see people who really don’t have a lot of money saved for when they hit that age, and all of a sudden their income declines, and they don’t have a lot of funds for an emergency or just to live day to day,” she says. “It’s never too late to start… Even in middle age, you can always look at budgeting and begin to create that cushion.”

No matter their circumstance or age, everyone should periodically take a look at their budgets and adjust accordingly, says Anderson. “Budgets change,” she says, for example, “when people have lost their jobs they think, ‘Now what do I do?’ It’s so critical in just about every phase in your life.”